Niche Real Estate For the Win

+ Q2 Income Fund Update = 8.1% distribution yield

Emerging real estate sectors continue to steal “market share” from traditional property types.

Office, strip centers, malls, hotels, etc. are not going extinct, but they are underperforming in absolute growth and return performance.

Niche (or alternative) real estate sectors are growing in importance in both public and private markets. We’re certain the below 2030 sector predictions for institutional real estate portfolios will be off; however, it’s highly probable these are directionally correct.

This is the simple thing about real estate investing vs. other assets: it’s glacial pace makes it easier to see where the puck is going.

Source: NCREIF & Nuveen

What gives us confidence in these private sector predictions?

Well, real estate public markets (REITs) are already there. In 2000, office assets were 20% of the total REIT market. Office is now just 7%. Those numbers are roughly the same for retail.

Private markets will slowly catch up as niche real estate classes continue to outperform.

Niche Real Estate / Sub Sector Examples:

Cold Storage - Industrial

Tech Real Estate - New Sector

Lab Space - Healthcare / Office

Build-to-Rent SFR & Manufactured Housing - Multifamily

Below are a few benefits to investing in these emerging asset classes. Each of these stems from a simple but undervalued point:

New yet proven strategies have far more room to grow (and margin for error) vs. established playbooks.

Reasons being:

Growing Demand - These new asset classes aren’t an accident: strong tenant demand willed them into existence.

Non-existent Supply - Since many niche asset classes are relatively young, existing supply is often insufficient to meet demand. There is a long runway before excess supply limits growth opportunities. Zoning approvals often provide a moat against over-building.

Superior Lease Terms & Business Models - Professional real estate firms have learned a few things over decades of managing assets. If and when new sectors emerge, property owners have leverage and set favorable lease terms, creating new standards that traditional real estate owners would kill for. For example, office owners would love to have all triple net leases, but that is not the historical norm. Traditional asset landlords and tenants are anchored to expensive lease conventions created 50+ years ago.

Reduced competition - the path to acquire and operate niche real estate is not clear. You often need to dig for information or fall backwards into a deal to get exposure to these sectors. This reduces the number of competitors and keeps cash flow returns higher until the sector is fully institutionalized.

Institutional Acceptance - eventually the cat inches then finally falls out of the bag. Investors rush in and outperforming niches become more accepted by investors last to the party (often pension and sovereign wealth funds). The cost of capital and exit cap rates steadily rerate and the intrepid early operators are rewarded. Yet, thanks to their unique business models, even mature niche sectors are still able to generate above average cash flow.

Takeaway & Recommendations: Follow the Money

High demand + low supply + fewer professional operators = goldilocks scenario for niche property owners & REIT investors.

This is why the capital trend is heavily weighted towards non-traditional real estate. Therefore, we recommend established operators in traditional sectors look to add a complimentary niche strategy.

Passive investors should look to gain exposure to new economy (niche) real estate vs. relying exclusively on traditional residential investments alone.

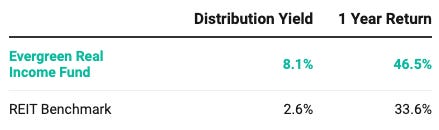

Evergreen Real Income Fund Update:

Q2 Performance:1

Our income strategy continues to outperform while providing monthly yields not achievable with the vast majority of liquid (public) and illiquid (private) options available today.

To learn more about the Evergreen Real Income Fund, click below:

If you are an accredited investor and would like to schedule a call to discuss, feel free to reply to this email.

MISC. Real Estate News

Canadian invasion: Tricon Residential just announced a joint venture to acquire $5 billion worth of single family homes across the sun belt. The Canadian firm already owns 25K homes. It seems ever major asset manager has or wants an SFR platform.

PE Firms never let a mega-trend go to waste: private-equity giant Carlyle Group Inc. is launching a $700 million venture to develop renewable power generation (solar) and storage projects

Real Estate Sector Recoveries: Traditional property sectors are experiencing dramatically different price recoveries:

Source2

Brad Johnson