Housing Crash Probability

Housing is the most important asset class by a country mile.

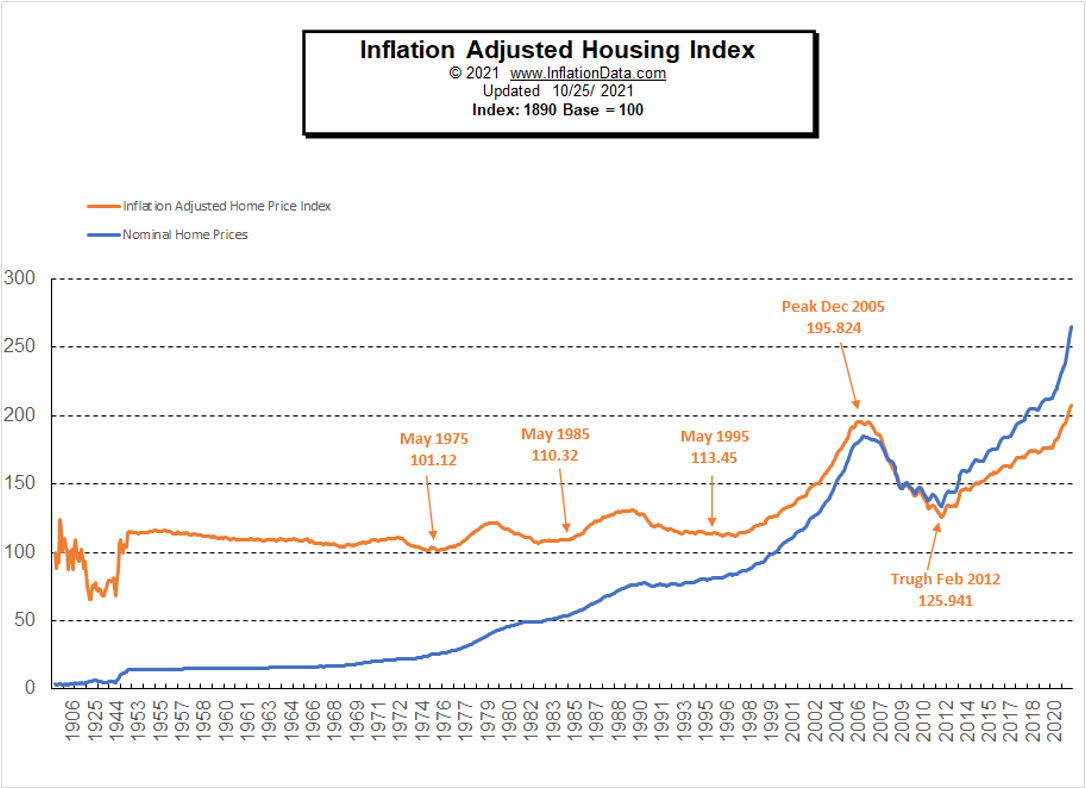

It’s so valuable that its health and 2nd order wealth effects impact every other asset class. This means few investors have the luxury to ignore housing when pricing gets wacky. Case in point: 2007.

Now, after a decade of steady gains and two years of parabolic increases, pricing is.…well, let’s just say it’s extended.

Nothing about the housing market feels sustainable right now. In two months mortgage rates mooned from 3% to 5%; one of the quickest rate increases on record. In the hottest markets, demand is so nutty that open houses look like music festivals.

But does that mean we’re in for another housing crash (30%+ decline)?

I highly doubt it.

To support that thinking… let’s do a top 5 list.

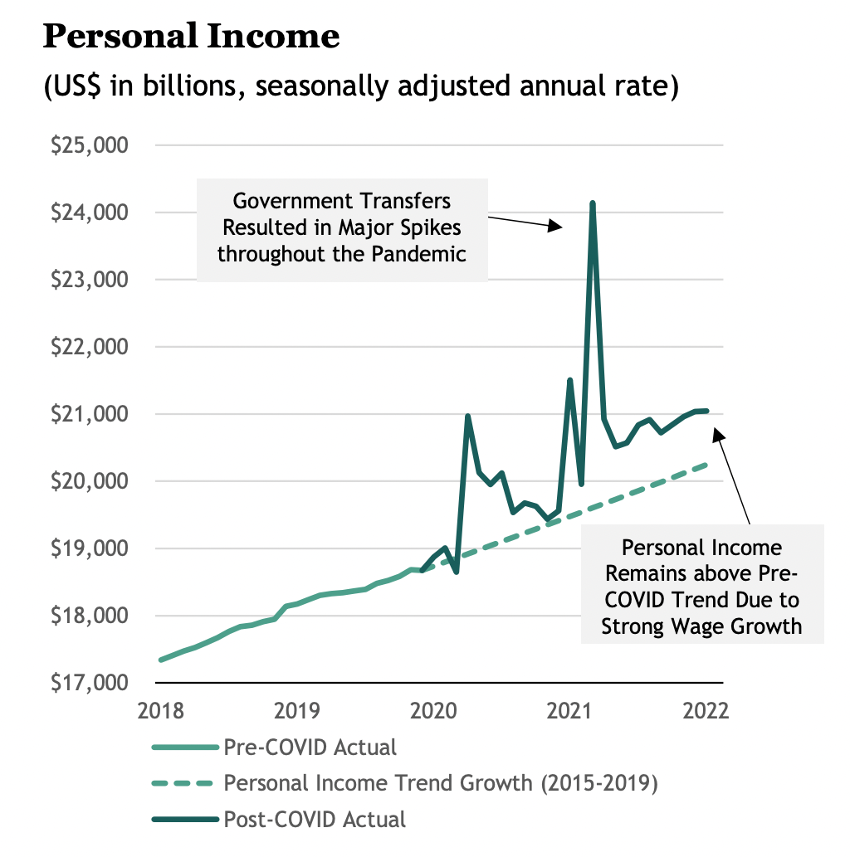

1. Most Americans Still Have Cash to Burn.

The average American’s balance sheet hasn’t been this strong in a long time. Two years of helicopter money from Washington + a dash of wage inflation means we’re all making more money. At least in nominal terms.

So mortgage payments are “full”, but so are the coffers1.

2. Existing Supply Low, New Supply SLOW

New housing permits are finally spiking. But permits don’t equal completions.

Homebuilders are making progress, but they are digging out of huge hole caused by the under-building overreaction to the last crisis.

We’re short on needed housing by (checks notes) a whopping 3 million units.

It will take years to make up for this shortfall and that’s without supply chain constraints, which we’re chock-full of today:

3. Homes Aren’t Being Used As Piggy Banks Like 2008

A whole lot of home owners refinanced at sub 3% mortgage rates. If this was you, its possible you might never refinance or move again.

Plus, this time banks weren’t stupid; they didn’t flood the market with refinance cash. They didn’t push leverage ratios to nosebleed levels like the subprime crash.

Remarkably, it appears consumers learned their lesson from the last crash and didn’t blow the extra savings. Well at least not all of the savings (boat sales spiked the last two years, but hey, we all desperately wanted to get outside).

4. Too Many SFR Investors At the Ready

Investors are purchasing 1 out of every 5 new homes for single family rentals. This sounds scary / reminiscent of the subprime crisis. However, these are not the same investors. Far from it. These aren’t highly leveraged, no-doc, just have a heartbeat type of borrowers. They are the largest and most sophisticated private equity investors in the world.

The have hundreds of billions to deploy into single family rentals (a relatively new asset class) and are ready to pounce on pricing weakness2.

5. How Long Can The Kids Live at Home?

The Millennial wave is here and they are entering peak home-buying age. 18% of millennials were living with their parents in 2020. Most want to start families and have their own space. I assume “Netflix and chill” is less cool sitting next to your snoring father on the couch. They have more savings and better jobs now, they are ready to buy.

If No Crash, Then What?

I don’t know, I’m not a housing expert. But who is? The “expert” housing economists are all over the map with their predictions.

What I do know is that for an asset to CRASH, you need a lot of forced sellers and few willing buyers.

Given the above factors, that’s not remotely close to the setup today.

What we do have is major supply chain issues, a lot of locked-in owners and a lot of desperate buyers. Prices could correct if rates don’t moderate, but it’s hard for me to imagine a non black swan scenario that kills housing over the short-term.

I think more probable (than a crash) is either a soft landing or a decline in real housing values vs. nominal. Which means that over the next few years housing may appreciate but might not keep up with inflation.

This is very similar to what happened in the early 1980’s, the last time inflation was ripping.

Barring an extreme outlier event, this seems to be the highest probability outcome for housing prices. We’ll see - either way, I’m not selling.

Thanks for reading,

Brad Johnson

Source: Blackstone, Bureau of Economic Analysis

Redfin Housing Market Data, Feb. 2022