"Toll Booth" Real Estate Investments

+ Industry Highlights (see bottom of email)

Invest once and collect growing income checks for 30+ years.

Sounds nice, right? These are our favorite type of investments. We think of them as “toll booths”. Not in the literal sense, but as a framework for high-margin real estate that compounds cash with little need for maintenance capital. In its purest form, a tollbooth investment is like royalty or property tax; the money only goes one direction.

All income, no hassles.

In other words, assets that produce durable income streams that outpace expenses and inflation. The opposite of a toll booth investment is a money pit. An asset where the GAAP income statements looks okay but it generates little to no actual cash flow. All operating income goes to pay for capital improvement expenses. Or worse, one unexpected maintenance project wipes out years of expected cash flow. Think of an office tower where the building systems fail or a major tenant vacates and their space needs a full retrofit.

That’s a trading asset, not a toll booth. That type of investment works if you time it right AND you have staying power (a lot of capital) to support the asset. These properties are fine to buy and flip, but they’re not great businesses.

Types Of Toll Booth Real Estate Plays

The following real estate niches exhibit toll booth characteristics:

Casino Real Estate (Ground Leases) – regulatory constraints on supply

Cell Towers – little maintenance, captive tenants (vital infrastructure)

Manufactured Housing Communities – ground leases, supply constraints

Self-Storage – near zero cap-ex, high margin cash flow (watch supply though)

Land Rights – 100% margin on royalties for land easements, water or mineral rights

Bio-Tech Hubs – typically triple net leases (few expenses) where the tenants are “pot committed” – they have invested heavily in the lab space / market

Common traits among these investments:

Stable or growing demand with rent inflation escalators

Mission critical facilities – landlord extracting value (toll fees) from much larger tenant revenue streams = landlord leverage

Low ongoing capital needs to maintain asset and rent growth

Supply constraints – typically caused by regulatory hurdles

Defense Wins Championships

While all four of these traits are desired, item 4 is the most important for long term holds. Without supply constraints, high cash flow yields should be competed away. Therefore, for generational holds, an asset must be defensible. If you can’t clearly define why the demand and supply equation will remain in your favor, it’s probably not going to be a lifetime hold.

To hold long term, you need to find assets that defy the slow entropy that plagues great businesses. The asset needs a unique structural advantage to sustain high profit margins and keep the competition at bay. This might be a niche asset class that flies under the radar or restricted zoning or use permitting. If supply is controlled, the tenant is denied options, which leads to predictable cash flows.

Higher Returns

Breaking news – our research confirms that high profit margins are typically better than low profit margins! Where do we collect our Nobel Prize in economics?

This sounds obvious because it is. But this rule isn’t written in stone. Amazon and Costco are lower margin businesses that focus on absolute dollar returns not profit margins. Yet, they’re both on the Mt. Rushmore of great businesses.

Of course, each have unreal cultures led by business geniuses. They made big bets, reinvested all cash flow and eventually reasonable – albeit low – profit margins materialized. However, they could have just as easily gone bankrupt pursuing such ambitious strategies.

Amazon in particular is the poster boy for survivorship bias. There are countless low margin companies that point to Amazon to justify lighting cash on fire (ex: WeWork). Few will be great investments.

It’s generally far safer to bet on highly profitable business models at fair valuations. The same is true for real estate. Favorable sectors with high margins don’t require brilliance; a golden retriever could run a toll booth.

Why? Because high margins solve a lot of problems. Plus there’s not much to do besides collecting cash. That frees up a lot of time and resources to focus on growing the business.

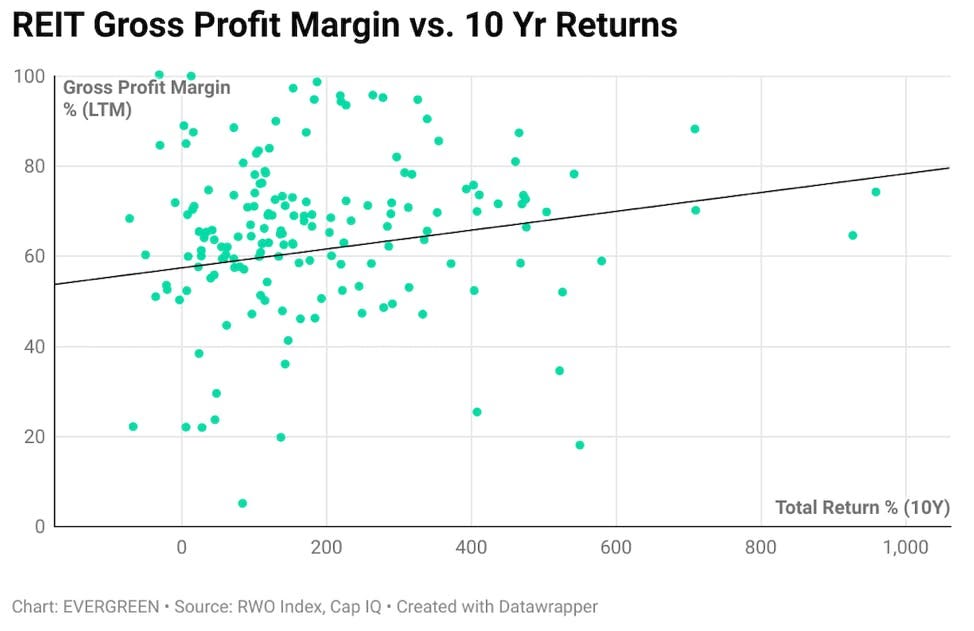

So, while not highly correlated, REITs with big margins do indeed generate superior returns. We don’t have the data to test yet, but we suspect this relationship strengthens when factoring in all prior recessionary periods. Reason being, such REITs are less dependent on debt markets (the kindness of strangers) during tough times.

As you can see in scatter plot above, low margin REITs can also deliver high returns. They just require a special characteristic to offset the higher expense handicap. Most likely, that’s an all-star acquisition team that drives returns through heroic growth.

We love firms that consistently drive solid deal flow. However, we’d rather not count on high octane acquisitions for our returns. Instead, we want REITs that pursue disciplined growth but still generate a lot of cash flow to increase our dividend checks.

We want toll booths.

Market Highlights

Despite nosebleed pricing, private real estate expected returns (6.4% on an unlevered basis) are still at a healthy spread relative to investment grade corporate (Baa) bonds (3.5%). So real estate expensive, but not on a relative basis. We’d expect this spread to tighten over the next few years.

Self Storage on Fire - move in rents are up 20% vs. pre-Covid and occupancy is at an all time high 95%+. Life changes & mobility are great for storage. New demand doesn’t seem temporary. The great reshuffling could help storage run hot until new supply can catch up.

Center of Gravity Shifting - Atlanta, Austin, Nashville, Tampa, Raleigh, and Charlotte are quickly becoming tier one markets for institutional investors.

Single Family Housing Rentals are the new darling of wall street. Everyone and their brother has a new SFR platform. Blackrock is even getting in the game.

Industrial - we’re currently in the best economic backdrop / market industrial owners have ever seen. Rent growth projected 8% nationwide in 2021 (11% coastal). New supply cannot keep up with demand. Distressed retail and office deals are possible conversion options, but nobody is doing this at scale. Industrial deals are catching 4% cap rate bids almost regardless of location.

Time to Upgrade Apartment Portfolios - the average cap rate spread between great to just okay multifamily markets hasn’t been this tight in decades. Unreal time to capitalize by selling older / outlier deals and rotate into high growth markets. Rare opportunity where selling high and buying higher actually makes sense.

$WRE (WashREIT) is dumping their DC office portfolio to Brookfield for an ~8% cap rate (83% occupancy). This is not a great look (comp) for Class B office owners. More distress pricing for office is likely on the horizon. Sunbelt office is a rare exception.

Brad Johnson