Case Study - Brookfield Property REIT

Below is REIT research Evergreen prepared to support our investment in the preferred shares of $BPYU (Brookfield Property REIT).

We don't make a habit of bragging about winners (as we'll obviously have our fair share of losers too). However, this case study is useful as it's indicative of how we think about risk vs. reward. Unfortunately, we don't believe anyone can properly quantify risk-adjusted returns, but this case study provides insights to how we think about those trade-offs.

In retrospect, we would have made a bit more money in the common units. However, we took far less risk in the preferred units. Despite the benefit of hindsight, we still believe this was the correct decision.

Assuming a viable vaccine, we assessed the loss of principal risk to the preferred units at ~1%. $BAM (holding in our total return strategy) is set to raise $100B across its various private equity strategies. They were not going to take the headline risk of defaulting on a (relatively) miniscule $240M preferred equity tranche that only required ~$15M of dividends to remain current.

Given $BAM's massive liquidity, the risk of principal loss to the common was still small, but an order of magnitude higher than the preferred.

Consequently, our income fund purchased the preferred shares in Q2 2020 at a big discount to par value with an ~9% yield on cost. We guessed it might take 1-2 years before the shares returned to par value. We were content to collect a well-protected ~9% coupon while we waited.

Today (1/4/2020) - Brookfield Asset Management (BAM) announced its intent to purchase 100% of BPY at 15% premium.

The preferred shares are now roughly valued at par. Considering the return potential is now limited to the coupon, we are now reducing the position and rotating the 31% profits (116% annualized) into our other long term holdings.

Analysis below:

--------

Investment Date - 8/21/2020

Brookfield Property REIT (BPYU) is a misunderstood stock that has been overly punished by the markets sell-off of all retail related stocks.

The REIT is managed Brookfield Asset Management, a $550 billion private equity firm which has near unlimited access to capital to support temporary cash flow shortfalls.

BPYU's preferred shares (BYPUP) is the safest way to invest in the firm, offering investors a substantial equity cushion, an ~9% coupon and 30% appreciation upside potential.

One way to generate outsized returns is to dig just a tiny bit deeper than the average investor. This is especially true with real estate investment trusts (REITs), as they tend to attract investors that love simplicity.

Brookfield Property REIT (BPYU) and its preferred shares are a great example of this dynamic. The ownership structure is more complicated than most REITs due to the massive size of the parent company Brookfield Asset Management, a $550 billion global asset management firm.

BPYU is a subsidiary of Brookfield Property Partners L.P. (BPY), which is Brookfields real estate division. BPY owns a portfolio of 122 retail properties, 136 office properties and various equity interests in diversified portfolio of manufactured housing, apartments, self storage and other class A commercial properties. BPY is a limited partnership that issues a K1 tax form to investors each year. BPYU is a REIT that issue a standard 1099-DIV tax form, which retail and non-taxable investors prefer.

BPYU, which technically only owns the retail assets, is effectively the same stock as BPY as shares can be exchanged 1:1 at anytime. BPY is a critical money maker for BAM, representing 34% of BAM's total invested capital.

We don't believe the market fully appreciates these facts and has unduly punished BPYU and it's preferred shares during this crisis.

BPY Ownership Structure

Source: BPYU, BPY

COVID-19 Is Crushing Brick-and-Mortar Retail

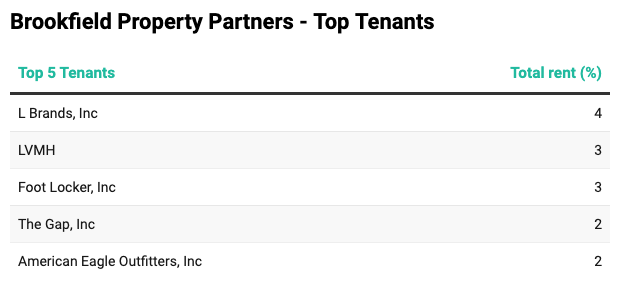

The retail industry was one of the worst affected industries following COVID-19 restrictions and lockdowns. Several mall retailers were forced to close their retail properties during Q2. This crisis follows several years of market share shift from the brick-and-mortar retail industry to the e-commerce industry. The rise in e-commerce industry has led to bankruptcies of several big retail names such as Forever 21, Fred’s and Toys”R”Us. The coronavirus pandemic further accelerated this trend. Several retail tenants have defaulted on rentals or are negotiating restructured contracts with rent concessions. Many of Brookfield’s top tenants such as Ann Taylor, The Gap and L Brands have announced store closures. High rent deferrals resulted in only 34% rent collection from BPYU’s tenants in Q2. There is no sugar coating it. It’s been a challenging year for the company.

Source: BPY’s 20-F filing

Positive Trends

While Q2 was difficult for the entire physical retail segment, underlying trends are recovering as lockdown restrictions have eased and people learn to live in the new normal. Nearly 15,000 tenants representing 85% of BPYU’s portfolio reopened their businesses and foot traffic is increasing. Not surprisingly, after recording historic declines in late March and April, retail store sales, as per census bureau, has rebounded the last 4 months, albeit not to pre-COVID levels.

Source: FT.com, U.S. Census Bureau

There is obviously strong secular growth in e-commerce; yet it would be rash to declare the demise of physical retail. In fact, while physical retail has lost share to online retail, in absolute terms, in-store retail sales actually saw an increase between 2016 and 2019. Retailers are adapting to the changing environment by introducing store pickup as well as using stores as returns & distribution centers.

Source: BPY’s Investor day presentation

Furthermore, US retail sales have quickly recovered from their April 2020.

Source: BPY’s Investor day presentation

BPYU’s Preferreds Are The Safer Bet

BPY owns extremely high-quality real estate, which tends to outperform coming out of a recession. We suspect the portfolio will fully recover. Yet, it is difficult to predict how many months or years that might take. Consequently, we believe the company's preferred shares are preferable over the short term.

It's reasonable to assume that BPYU’s common stock might experience high volatility given the elevated economic uncertainties. We believe that makes the preferred stock the superior near-term risk / reward option.

The cumulative and perpetual preferred stock (BPYUP) has a coupon rate of 6.375% p.a. and is trading at $18.79 , resulting in an attractive 8.5% yield with potential for ~30% capital appreciation should the preferred shares return to par value.

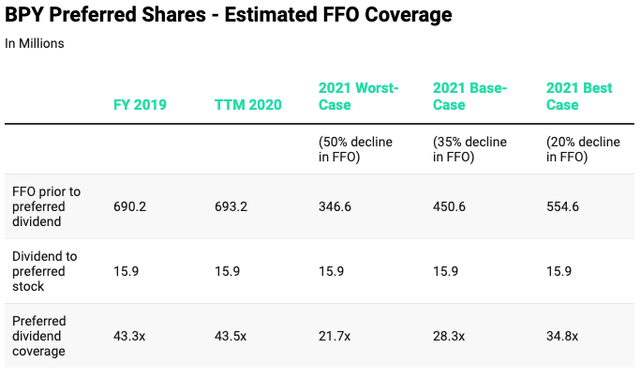

Despite COVID-led retail dislocation, the company’s Funds from Operations (FFO) can easily cover preferred dividends for the foreseeable future. As indicated in the table below, we've projected BPYU’s FFO for the next twelve months. Even in the worst-case scenario of 50% FFO decline, preferred dividend coverage is expected to be 21.7x. Also, BPY’s decision to cut 20% of its retail arm’s workforce should improve net cash flows, thereby improving coverage further.

Source: BPYU’s filings, Evergreen

Investors should note that while FFO increased in H1 2020, its cash flow from operations (CFO) was -$154.6M in H1 2020 compared to $101.3M in H1 2019. This was due to deferred rent payments stemming from the pandemic. We view the CFO shortfall as temporary considering a large portion of the company’s tenants were not operating in Q2 2020.

Ample Liquidity & Flexibility to Weather the Storm

The company's strong balance sheet has supported its near-term liquidity challenges. As of June 2020, BPYU had $210M in cash and $415M available under its revolver. After a common share buy-back of $88M (a strong vote of confidence from management), the company's direct liquidity stands at $537M.

The company has a total debt of $16.8B out of which $3.55B is maturing during the remainder of 2020 and 2021. This near-term debt maturity schedule is troubling for some investors as they assume BPY will not be able to refinance debt given the crisis.

We believe those concerns are overblown.

According to Brian William Kingston, CEO of Brookfield Property Partners on the Q2 2020 earnings call:

Debt markets are open and accessible to high-quality borrowers secured by strong assets. In the second quarter alone, we financed, refinanced or extended mortgages on nearly $2.1 billion of office, retail and multifamily properties at interest rates that were, on average, below 4%. We ended the quarter with just under $6 billion of group-wide liquidity.

Source: Brookfield Property Partners L.P., Q2 2020 Earnings Call, Aug 06, 2020

The ability to access more than $2 Billion of debt during the peak of pandemic fears is a strong testament to the marketplace's confidence in Brookfield's business and assets.

Furthermore, the vast majority of BPY's debt is single-asset, non-recourse, meaning that - if needed - the company can walk away from debt on assets that were already struggling prior to COVID. Mr. Kingston notes:

Now within our portfolio, we have 180 malls and over 200 office buildings. And so this is a very small number by number of assets and certainly by the amount of equity that we have invested in them, it's immaterial. And so it's just really allowing us to, as you say, either restructure the loans in some format or, in some cases, just relieve ourselves of that debt obligation, where it no longer makes sense to continue funding the shortfalls in those assets.

Source: Brookfield Property Partners L.P., Q2 2020 Earnings Call, Aug 06, 2020

Also, BPYU is backed by a leading alternative asset manager and world’s largest real estate company, Brookfield Asset Management (“BAM”) which has enough capital to support the retail business as it fights near-term headwinds.

BPYU accounts for nearly 42% of the total invested capital of the parent company, making it a crucial part of the business. BAM is ready and able to support its retail arm with its whopping $6B of available liquidity.

Finally, BAM is looking to raise $100B across its variou business lines, including a $12.5B credit fund that can actual purchase BPY's mortgages - at likely a compelling discount - if needed.

Source: BPYU’s filings

Most companies do not have this level of flexibility with investor funds. However, BAM has proven to be an impressive capital allocator. Consequently, its investors have given them wide discretion on how to best compound capital.

BAM's main economic driver is its ability to raise massive funds. What is the likelihood that Brookfield wants the negative press associated with defaulting on a $240M preferred share? Plus, the preferred obligation is only $15M / year, which is a rounding error for a firm with $6B in liquidity. We believe the probability of a preferred default, while not zero, is extremely low.

Furthermore, in addition to the preferred distributions, BPY is already paying common shareholders $569M per year in dividend payments. While BPY could certainly announce a reduction in the dividend to its common holders, that is still a sizable margin of error for the preferred holders.

** WE EXITED THIS POSITION WHEN THE PREFERRED SHARES RETURNED TO PAR VALUE **